Penetration Testing for Fintech Companies in Australia: The Stakes Have Changed

A few years ago, a fintech startup in Sydney or Melbourne could launch a product, serve thousands of customers, and worry about security "later." That window has firmly closed.

Today, Australian fintech companies sit squarely in the crosshairs of regulators, sophisticated threat actors, and a customer base that has become acutely aware of what a data breach means for their financial lives. The Australian Prudential Regulation Authority (APRA), the Australian Securities and Investments Commission (ASIC), and the broader Consumer Data Right (CDR) framework have collectively raised the bar in ways that cannot be ignored.

Penetration testing has become the backbone of how serious fintech companies demonstrate security maturity. Not because a checklist demands it, but because the threat landscape, the regulatory environment, and the trust economy all require it.

This is what Capture The Bug works through with fintech clients across Australia every week, and this blog breaks down what the regulatory picture actually looks like, what best practices mean in the real world, and why security testing done right is a competitive advantage, not just a compliance burden.

What Australian Regulators Actually Expect

The regulatory framework for fintech security in Australia is not vague. APRA Prudential Standard CPS 234 is the clearest signal the regulator has sent to any entity it supervises, and its influence has rippled well beyond traditional banks into fintechs holding Australian Financial Services Licences (AFSLs) or operating under Banking-as-a-Service arrangements.

CPS 234 requires that regulated entities maintain information security capabilities that are proportionate to the threats they face. It demands that security controls be tested regularly and that the results of those tests be acted upon. Penetration testing is explicitly recognised as one of the core mechanisms for validating that controls actually work, not just that they exist on paper.

ASIC has separately published guidance reinforcing that cyber resilience is a board-level responsibility, not an IT department issue. When ASIC reviewed the cyber practices of financial services companies in its 2023 report, it found that many organisations had controls they believed were working but had never actually tested under realistic conditions.

For fintechs participating in the Consumer Data Right ecosystem, the CDR security profile imposes additional obligations around data holder security, and the ACCC and Data Standards Body both expect demonstrated security practices from accredited participants. The bottom line is that Australian regulators are not looking for fintech companies to claim they are secure. They are looking for evidence, and penetration testing provides that evidence.

Why Fintech is a High-Value Target

Fintech companies handle what attackers want most: payment credentials, bank account data, identity documents, and transaction histories. A single compromised API endpoint in a buy-now-pay-later platform or a poorly secured mobile banking application can expose tens of thousands of customer records in hours.

What makes fintech particularly exposed is the speed at which products are built and shipped. Features get released, third-party integrations get added, and the attack surface grows faster than internal security teams can track. This is not a criticism; it is the nature of building in a fast-moving sector.

The challenge is that attackers understand fintech architecture. They know how open banking APIs work. They know the common misconfigurations in payment gateway integrations. They understand how session tokens behave in mobile applications and where authentication logic is most likely to break under pressure. Capture The Bug works with fintech companies precisely because fintech requires testers who understand the domain, not just the testing methodology. A penetration test on a payments platform is fundamentally different from a test on a retail website, and the findings that matter most are the ones that connect directly to financial data flows and customer account integrity.

What Penetration Testing for Fintech Actually Covers

A well-scoped penetration test for an Australian fintech company is not a single exercise. It is a structured programme that maps to the company's product surface, data flows, and the specific regulatory obligations it carries.

The most critical testing areas for fintech include the following:

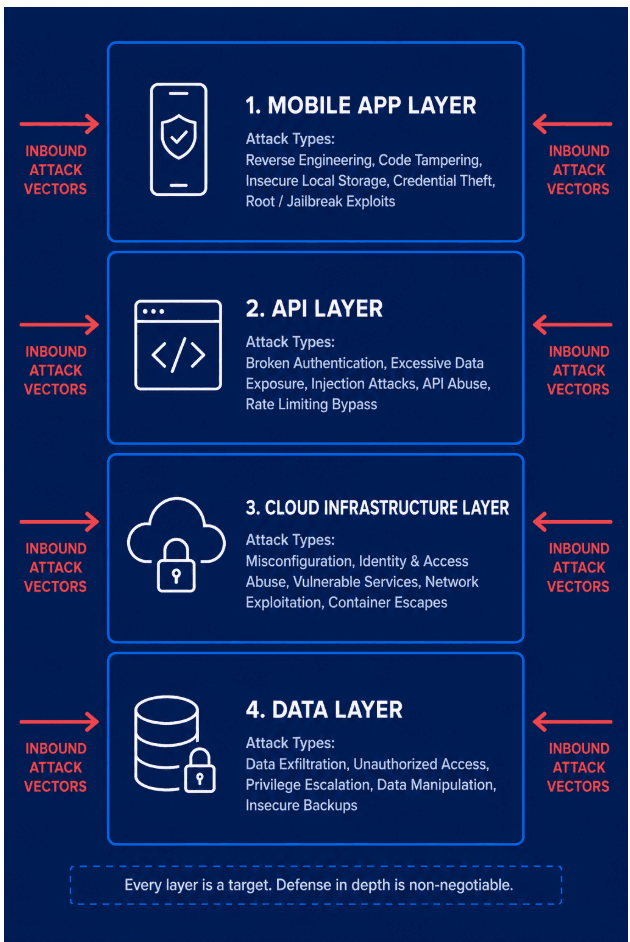

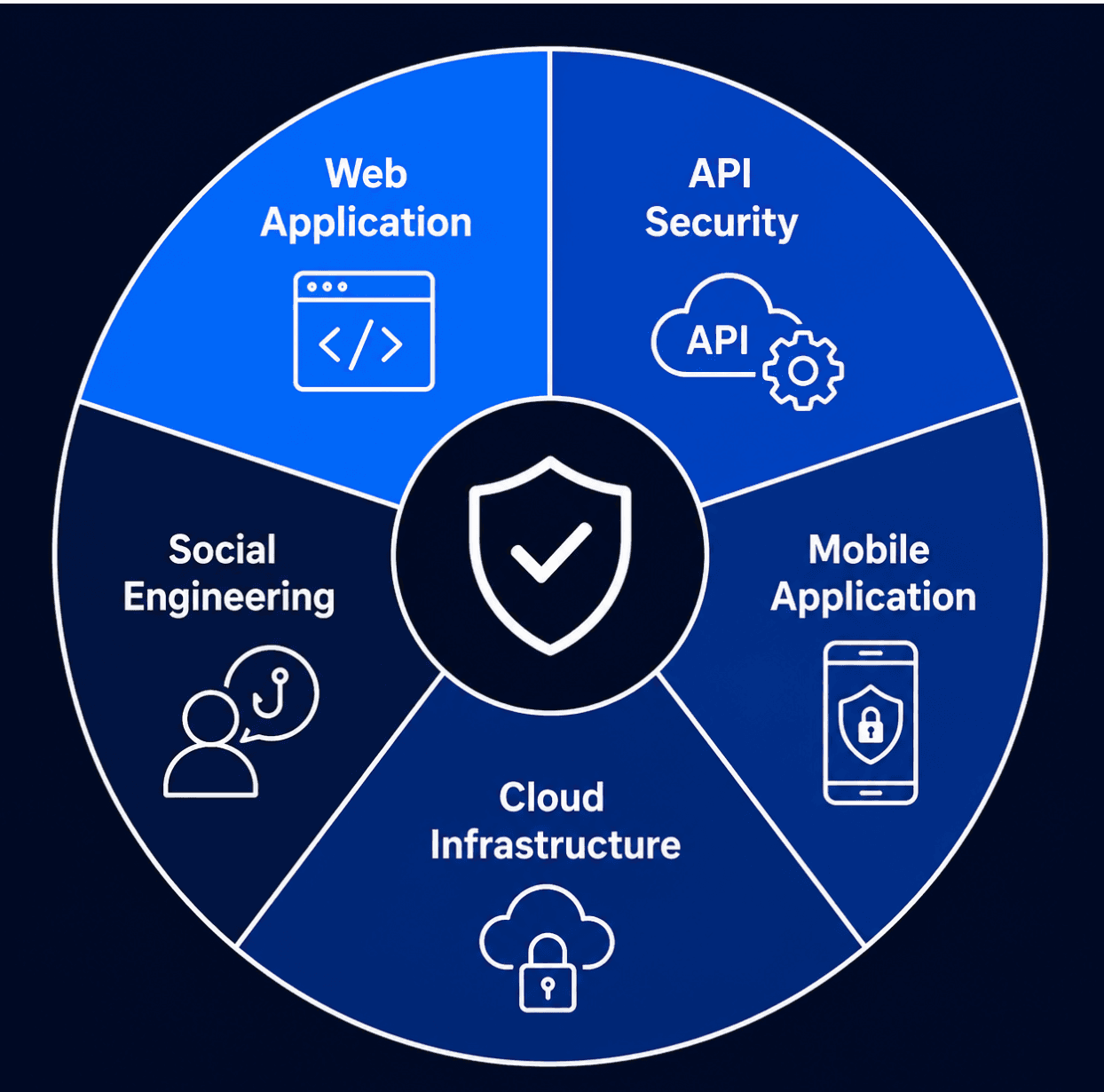

Web Application Testing: Most fintech products are delivered through web applications and mobile apps. Testing covers authentication mechanisms, session management, access controls, and how financial data is handled. Common findings include broken object-level authorisation, insecure direct object references, and inadequate controls around high-value transactions.

API Security Testing: Open banking, payment APIs, and partner integrations are where fintech companies are most exposed. APIs that expose balances, initiate payments, or handle identity verification require rigorous testing. Capture The Bug's penetration testing services are specifically designed to probe these surfaces under realistic conditions.

Mobile Application Testing: Whether consumer-facing or business banking, apps introduce distinct risks. Certificate pinning, local storage, session handling, and inter-app communication carry vulnerabilities commonly exploited in the wild.

Infrastructure and Cloud Testing: Fintechs running on AWS, Azure, or GCP often inherit a false sense of security. Misconfigured storage buckets, overpermissioned service accounts, and exposed administrative interfaces are common findings.

Social Engineering and Phishing Simulations: Human risk is consistently underestimated. Testing whether employees would hand over credentials or click on convicing phishing emails is as crucial as testing the software code.

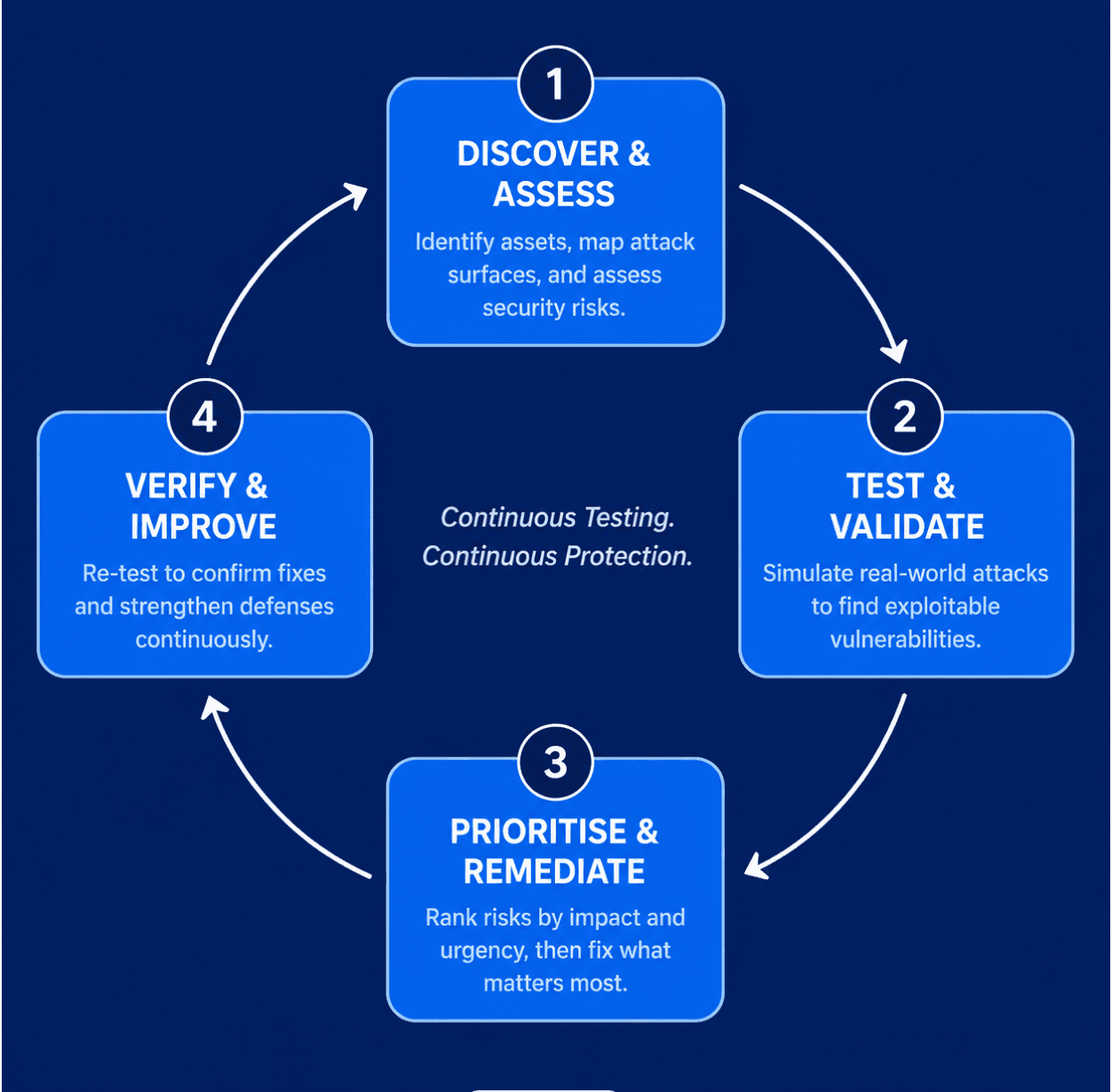

Best Practices for Fintech Security Testing

Understanding what needs to be tested is one thing. Building a programme that actually delivers lasting security improvement is another.

Test with real-world objectives in mind. The most valuable penetration tests are scoped around what an attacker would actually want to achieve: accessing customer funds, extracting identity data, manipulating transaction records, or gaining persistent access. Generic testing produces generic findings. Objective-based testing produces findings that the board and regulators can act on.

Test more than once a year. Annual testing was acceptable when fintech products changed slowly. Today, shipping updates regularly requires a testing cadence that reflects the pace of change. Capture The Bug works with fintech clients on ongoing security testing programmes because the threat picture does not pause.

Take remediation seriously. A penetration test that produces a report and nothing else is a compliance exercise. The findings from a test should drive specific, prioritised remediation, and a retest should confirm that the issues have been resolved correctly.

Involve the right stakeholders. Testing findings should reach the CISO, the CTO, and the board. Regulatory expectations in Australia are explicit that cyber risk governance is a leadership responsibility. When results are shared only within the engineering team, they lose the organisational weight needed.

Document everything for regulators. APRA, ASIC, and CDR auditors will ask for evidence of security testing. A well-maintained record of penetration test reports, remediation tracking, and retest outcomes is one of the clearest ways a fintech company can demonstrate security maturity.

CREST Certification and Why It Matters in Australia

Not all penetration testing providers are equivalent, and in Australia's regulated financial services environment, the provider a fintech company chooses carries real weight.

Capture The Bug holds CREST certification, which is the internationally recognised standard for penetration testing quality and professional conduct. For Australian fintech companies operating under APRA oversight or engaging with CDR accreditation requirements, working with a CREST-certified provider is increasingly expected and, in some cases, explicitly required by regulatory obligations.

CREST certification means that the methodologies, the people, and the quality controls behind the testing meet a verified standard. For fintech companies that are growing their enterprise sales, many large financial institutions and corporate customers now require CREST-certified testing as a condition of partnership. Choosing the right provider from the beginning saves the rework of having to redo testing later.

Conclusion: Security Testing is a Growth Decision

Australian fintech companies that treat penetration testing as a checkbox eventually find themselves in one of two places: facing a regulator who is asking hard questions about a breach, or winning enterprise customers because they can demonstrate a mature security programme their competitors cannot.

The fintech companies that are winning trust with customers, regulators, and enterprise partners are the ones who can prove their product is secure and back it up with evidence. That starts with a penetration test done properly. Learn more about Capture The Bug's fintech penetration testing services at capturethebug.xyz/Services/penetration-testing.

Plan Your Annual Pentesting Strategy the Right Way

Learn how modern SaaS companies structure pentesting across the year to reduce risk, stay compliant, and avoid last-minute panic before audits.

Frequently Asked Questions

Is penetration testing required for fintech companies in Australia?

Yes. Under APRA Prudential Standard CPS 234, regulated entities must regularly test their security controls, and penetration testing is one of the primary ways this requirement is fulfilled. Fintech companies operating under an AFSL or within the CDR ecosystem are expected to demonstrate active and documented security testing as part of their compliance obligations.

How often should a fintech company in Australia conduct penetration testing?

Most Australian regulators and industry frameworks recommend at least annual penetration testing as a baseline. However, fintech companies that release product updates regularly, onboard new integrations, or handle significant volumes of financial data benefit from more frequent testing. Capture The Bug works with fintech clients on ongoing testing programmes tailored to their pace of development and risk profile.

What does a penetration test for a fintech company typically cover?

A fintech-focused penetration test typically covers web applications, mobile applications, payment and open banking APIs, cloud infrastructure, and internal network environments. The scope is shaped by the specific product architecture and the data flows that carry the highest regulatory and financial risk.

Why does CREST certification matter when choosing a penetration testing provider for fintech?

CREST certification ensures the penetration testing provider meets a verified international standard for methodology, professional conduct, and quality assurance. For fintech companies subject to APRA oversight or engaging enterprise clients in financial services, working with a CREST-certified provider like Capture The Bug provides assurance that the testing is credible and the findings are defensible to regulators and auditors.

What is the difference between a vulnerability assessment and a penetration test for fintech?

A vulnerability assessment identifies and classifies potential weaknesses in a system. A penetration test goes further by actively attempting to exploit those weaknesses to determine what an attacker could actually access, extract, or compromise. For regulatory purposes and real-world risk management, fintech companies need penetration testing, not just vulnerability assessments.

How does penetration testing support APRA CPS 234 compliance?

CPS 234 requires entities to maintain and regularly test information security controls in a way that is proportionate to the risk they carry. Penetration testing directly satisfies the testing obligation by providing documented evidence that controls have been evaluated against realistic attack conditions. A well-maintained record of penetration test reports and remediation outcomes is one of the strongest indicators of CPS 234 compliance during an APRA review.